Introduction

If you’re building automation systems for mortgage brokers inside GoHighLevel, compliance isn’t optional it’s foundational. One misstep in messaging, AI automation, disclosures, or SMS campaigns can put your client’s license at risk.

That’s why every GHL agency serving loan officers needs a clear, practical mortgage compliance guide—not legal theory, but real-world steps you can implement inside your snapshots, funnels, and workflows.

This guide walks you through how to stay compliant while still leveraging automation, AI receptionists, SMS follow-ups, and marketing funnels to grow your mortgage clients’ businesses confidently.

Key Takeaways

- Compliance must be built into your snapshot from day one

- A2P 10DLC registration is mandatory for mortgage SMS campaigns

- AI chatbots and voice AI must avoid unlicensed advice

- All funnels should include required NMLS disclosures

- Automated marketing must follow consent and opt-in rules

- Email sender settings and domain setup impact compliance

- Documentation and audit trails protect both agency and client

Why Mortgage Compliance Matters More in GHL

Mortgage marketing is highly regulated. Loan officers operate under federal guidelines such as RESPA, TILA, and state-level licensing requirements. When you introduce automation, AI responses, SMS campaigns, and drip sequences, the compliance surface area expands dramatically.

As a GHL agency, you’re not just providing software you’re building systems that:

- Capture borrower data

- Send rate information

- Trigger SMS campaigns

- Automate follow-up sequences

- Use AI to respond to borrower questions

Without structure, these automations can unintentionally violate compliance standards.

A strong mortgage compliance guide ensures your automation enhances trust instead of creating liability.

The Foundation of a Mortgage Compliance Guide

Before diving into tools, you need core compliance pillars built into your agency process.

Clear Consent and Opt-In Rules

Mortgage leads must explicitly opt in to receive communication. That means:

- Checkbox consent on all forms

- Clear SMS and email opt-in language

- Terms and Privacy Policy pages

- Proper opt-out instructions in SMS

Inside GHL, ensure:

- All forms include consent language

- Workflows only trigger after verified opt-in

- SMS messages include “Reply STOP to opt out.”

Never import cold lists into SMS campaigns. That’s not just risky; it’s illegal under A2P standards.

Ready to bring your 24/7 Mortgage Chatbot to life?

Get the Mortgage Snapshot today and start closing more loans.

A2P Registration and SMS Compliance

If your mortgage clients send SMS to U.S. numbers, they must complete A2P 10DLC registration.

Here’s how agencies should handle it:

Step 1: Brand Registration

Register the mortgage business brand through The Campaign Registry.

Step 2: Campaign Registration

Define what type of messages will be sent:

- Appointment reminders

- Loan status updates

- Marketing offers

- Follow-ups

Be accurate. Misrepresentation causes rejection.

Step 3: Ongoing Monitoring

Avoid prohibited content

- Don’t send misleading rate claims

- Keep opt-out language active

Pro tip: Build A2P registration into your onboarding checklist.

AI Automation Without Compliance Risk

AI receptionists and chatbots are powerful but risky if misconfigured.

- Mortgage AI should:

- Gather information

- Schedule appointments

- Provide general process guidance

It should NOT:

- Offer personalized rate advice

- Quote exact loan terms

- Guarantee approvals

- Interpret underwriting outcomes

Safe AI Prompt Framework

Instead of saying:

“You qualify for a 5.75% rate.”

Use:

“Rates vary based on credit profile and market conditions. A licensed loan officer will review your details.”

This small shift protects your client’s license.

Your Mortgage Compliance Guide should include standardized AI prompts that every sub-account uses.

Email Compliance for Mortgage Agencies

Email compliance is often overlooked.

Here’s what your agency must ensure:

- Accurate sender name

- Business domain email

- Physical mailing address in footer

- Clear unsubscribe link

Inside GHL workflows:

- Configure sender email properly

- Avoid misleading subject lines

- Don’t exaggerate rates

Data Privacy and Secure Handling

Mortgage leads contain:

- Social Security numbers

- Income data

- Employment information

- Credit score ranges

Never store full sensitive financial details inside open text fields unnecessarily.

Recommendations:

- Use secure 1003 form integrations

- Avoid asking for full SSN via chatbot

- Restrict user permissions in GHL

- Limit access to pipelines

Your mortgage compliance guide should also define the following:

- Who can export contacts

- Who can access notes

- How long data is retained

Workflow Best Practices for Compliance

Automation can create accidental violations if not structured properly.

Here’s a safer workflow model:

- Lead submits compliant opt-in form

- Immediate confirmation message

- Short nurture sequence

- Appointment booking

- Loan officer review

Avoid:

- Long aggressive SMS blasts

- Daily rate push campaigns

- Unverified marketing claims

Instead, focus on:

- Education-based nurture

- Appointment-driven messaging

- Status updates

Compliance and conversion can coexist.

Referral and Review Campaign Compliance

Mortgage referrals must avoid illegal incentive structures.

You can:

- Ask for reviews

- Request referrals

- Provide general appreciation

You cannot:

- Offer undisclosed cash incentives

- Tie referral rewards to loan closing

- Misrepresent borrower experience

Record Keeping and Audit Protection

Agencies often overlook documentation. Protect yourself and your client by:

- Saving AI prompts used

- Archiving workflow versions

- Logging consent timestamps

- Storing A2P approval documentation

If a regulator investigates, audit trails matter.

Create a compliance folder in your agency drive for every mortgage client.

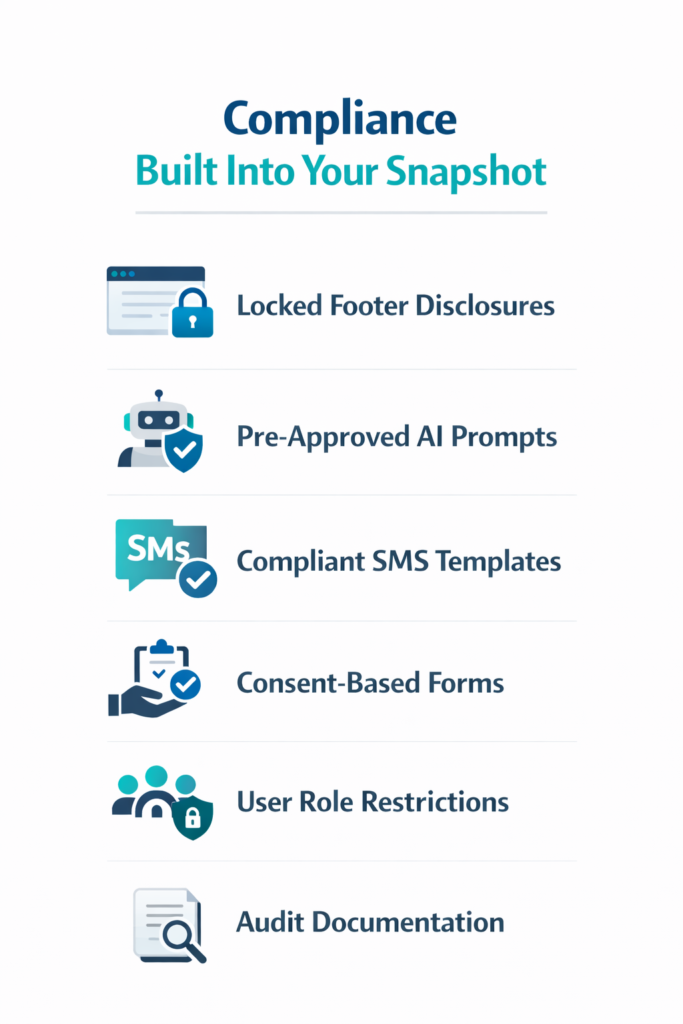

Building Compliance Into Your Snapshot

The smartest GHL agencies bake compliance into their snapshot.

Your mortgage snapshot should include:

- Locked compliance footer

- Pre-written AI prompts

- Approved SMS templates

- A2P-ready messaging flows

- Consent-based forms

- Compliant email templates

- Restricted user roles

This reduces human error dramatically. Compliance should not depend on the loan officer remembering details.

Frequently Asked Questions

Do GHL agencies need to be licensed to serve mortgage clients?

No, but you must avoid giving mortgage advice or structuring loan terms. Your role is technology provider, not loan originator.

Can AI quote mortgage rates automatically?

It should not provide personalized rate quotes. Keep responses general and direct borrowers to licensed professionals.

Is A2P registration mandatory?

What disclosures must be on a mortgage funnel?

At minimum:

- NMLS ID

- Legal company name

- Equal Housing Lender logo

- Privacy Policy

- Terms & Conditions

Can mortgage clients run Facebook lead ads?

Yes, but ad copy must avoid misleading guarantees and include compliant disclosures.

Conclusion

Scaling mortgage automation inside GoHighLevel is incredibly powerful — but only when done responsibly.

A clear mortgage compliance guide protects the following:

- Your agency

- Your client’s license

- Their reputation

- Their long-term growth

Automation should amplify credibility, not introduce risk.

If you build compliance into your snapshot from the beginning, consent forms, AI guardrails, proper disclosures, and documented workflows you create something far more valuable than software.

You build a secure, scalable lending system that wins trust while increasing conversions.